What Does a Bid Bond Mean for Subcontractors?

Discover what a bid bond means for subcontractors and how it impacts your project pursuits. Enhance your understanding and boost reliability!

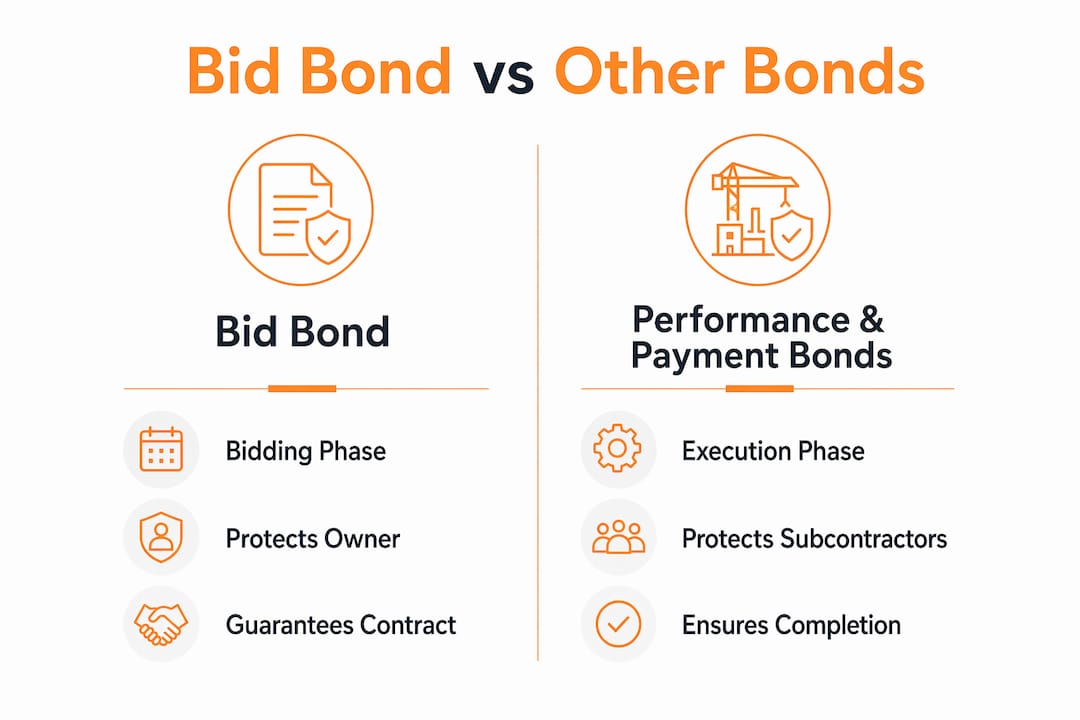

A bid bond is a surety bond that guarantees a contractor will enter into a contract at the submitted bid price and provide the required performance and payment bonds if awarded the project. For subcontractors, understanding what a bid bond means is not optional knowledge. It directly affects which projects you can pursue, how general contractors evaluate your reliability, and what obligations you carry from the moment you submit a bid. The term “bid bond” is the recognized industry standard, and it sits at the front of every bonded construction project’s paperwork sequence.

What does bid bond mean for subcontractors?

A bid bond is a three-party agreement between the contractor (principal), the surety company, and the project owner (obligee). The surety company backs the contractor’s promise to honor the bid. If the winning bidder refuses to sign the contract or cannot produce the required follow-up bonds, the owner files a claim capped at the bond amount. That claim compensates the owner for the cost difference between the defaulting bid and the next lowest bid.

For subcontractors, the bid bond explanation starts here: you are rarely the party posting the bid bond. The prime contractor (general contractor) typically submits the bid bond to the project owner. But your work, your pricing, and your bonding capacity can all influence whether the prime’s bid bond holds up after award. That indirect exposure is what makes bid bond literacy so critical for subs.

The bid bond amount is usually set at 5% to 10% of the total bid price, though public projects sometimes require higher percentages. This figure is not a cost you pay upfront. It is a guarantee backed by the surety, and the surety will underwrite the prime’s financial strength and project history before issuing it.

How bid bonds differ from performance and payment bonds

The bonding sequence in construction follows a clear order, and confusing the three bond types is one of the most common mistakes subcontractors make. Bid bonds transition to performance and payment bonds after contract award. Each bond covers a different phase and a different risk.

| Bond Type | When It Applies | Who It Protects | What It Covers |

|---|---|---|---|

| Bid bond | Bidding phase only | Project owner | Contractor honoring bid price and providing follow-up bonds |

| Performance bond | Construction phase | Project owner | Project completion per contract terms |

| Payment bond | Construction phase | Subcontractors and suppliers | Payment for labor and materials |

The bid bond covers intent and financial capability at the bidding stage only. Once the contract is signed and the performance and payment bonds are issued, the bid bond’s job is done. A performance bond then guarantees the project will be completed according to contract specifications. A payment bond protects subcontractors and material suppliers from nonpayment by the prime contractor.

This distinction matters enormously for subs. You are not a direct beneficiary of the bid bond. Your payment protection comes from the payment bond, which is a separate instrument issued after award. Subcontractors who assume the bid bond covers them if the prime fails to pay them are operating on a dangerous misunderstanding.

Pro Tip: When you receive a bid invitation, look for the bonding section and identify whether the project requires a payment bond. That bond, not the bid bond, is your financial safety net during construction.

The bid tabulation process also connects to bonding. If a prime’s bid is disqualified for failing to submit a proper bid bond, every subcontractor who priced that bid loses the opportunity. Your exposure to the prime’s bonding compliance is real, even when you never touch the bond paperwork yourself.

When subcontractors might need to be named on a bid bond

Most subcontractors do not post their own bid bonds. But “most” is not “all,” and the exceptions matter. Some public project bid documents require subcontractors to be named on the prime’s bid bond or to provide proof of surety coverage at bid submission. Bid notices can require subcontractor surety proof before the prime’s bid is considered complete.

Here is what to look for when reviewing bid documents:

- Subcontractor naming requirements. Some bids require the prime to list major subcontractors by name and trade, with confirmation that each sub has bonding capacity or is covered under the prime’s bond.

- Surety proof at submission. Certain public agency bids, particularly in states like New Jersey, require subcontractors to submit proof of bonding capability alongside the prime’s bid package.

- Subcontractor-specific bond thresholds. Federal projects governed by the Miller Act require payment and performance bonds on contracts over $150,000. State “Little Miller Act” equivalents vary by jurisdiction and can impose bonding on subcontractors directly.

- Prime contractor requirements passed downstream. Many general contractors require subcontractors to provide their own performance and payment bonds when the subcontract value exceeds a set threshold, often $100,000 or more.

- Bid document bonding clauses. These clauses specify whether the prime’s bond covers subcontractors or whether subs must arrange separate surety coverage.

Early coordination with the GC’s surety and bonding broker reduces surprises. If you are a named subcontractor on a large public bid, the surety may request your financial statements, work-in-progress schedules, and credit history before the bid is submitted. Preparing that documentation in advance keeps the prime’s timeline intact and signals your professionalism.

Pro Tip: Request a copy of the full bid document, not just the scope of work, before pricing any public project. The bonding section is often buried in the general conditions and easy to miss.

Common misconceptions subcontractors have about bid bonds

The most persistent misconception is that a bid bond guarantees the project will be completed. It does not. Bid bonds guarantee contract signing and the supply of required follow-up bonds, nothing more. Once the prime signs the contract and delivers the performance bond, the bid bond has fulfilled its entire purpose.

A second misconception is that subcontractors benefit directly from the bid bond if something goes wrong. They do not. The bid bond’s sole beneficiary is the project owner. If the prime walks away after winning the bid, the owner collects from the surety. Subcontractors who have already mobilized, ordered materials, or allocated crews have no claim against the bid bond.

“Bid bond claims arise when a contractor refuses to sign the contract or cannot provide the required performance and payment bonds after award. They have nothing to do with construction performance or payment to subcontractors.” — Autodesk Construction Blog

Two additional risks deserve attention:

- Double bonding exposure. When a prime requires a subcontractor to provide their own performance and payment bond, the sub bears the cost of that bond and the underwriting scrutiny that comes with it. Subs with thin financials or limited bonding history may find themselves priced out of bonded work.

- Surety underwriting at bid stage. Surety underwriting reduces the risk of contractors underbidding beyond their financial capacity. If a prime’s surety has concerns about a named subcontractor’s financial health, that sub may be replaced before the bid is submitted. Your bonding capacity is effectively a prequalification filter.

Understanding these risks is not pessimism. It is how experienced subcontractors protect their pipelines. Reviewing bid tracking software benefits can help you monitor which bonded projects you are pursuing and flag bonding requirements before they become last-minute problems.

Practical tips for subcontractors navigating bid bond requirements

Managing bid bond requirements does not require a law degree. It requires a disciplined process applied consistently across every bid you pursue.

- Read the full bid solicitation before pricing. The bonding section, general conditions, and special provisions all contain requirements that affect your obligations. Skipping to the scope of work and drawings leaves you exposed.

- Contact the general contractor’s bonding broker early. If you are a named subcontractor on a bonded public bid, ask the GC who their surety is and what documentation they need from you. Waiting until bid day creates unnecessary pressure.

- Prepare your financial package in advance. Sureties typically review two to three years of financial statements, a current work-in-progress schedule, and a bank reference. Having these documents ready shortens the underwriting timeline.

- Know your bonding limit. Every subcontractor has a practical bonding capacity based on their financial strength. Pursuing projects that exceed your surety’s comfort zone leads to declined bonds and lost bids. Talk to your bonding broker annually to understand your current limit.

- Clarify subcontract bonding requirements before signing. If the prime requires you to provide your own performance and payment bond, factor that cost into your bid. Bond premiums typically run between 0.5% and 3% of the contract value, depending on your financial profile and the project type.

Pro Tip: Ask your surety broker to review the bid documents with you on any public project over $500,000. They will identify bonding obligations you might miss and can advise on whether the project fits your current bonding capacity.

The detailed takeoff process also connects to bonding readiness. Accurate quantity takeoffs produce tighter bids, which reduce the risk of underbidding and the downstream bonding complications that follow when a project runs over budget.

Surety bonds protect public funds and assure project owners that contractors are qualified. For subcontractors, building a track record with a surety company is a long-term investment in your ability to compete on larger, higher-margin projects.

Key takeaways

A bid bond guarantees a contractor will sign the contract and deliver performance and payment bonds after award. It does not protect subcontractors from nonpayment or guarantee project completion.

| Point | Details |

|---|---|

| Bid bond definition | A surety bond guaranteeing the prime will sign the contract and provide follow-up bonds if awarded. |

| Subcontractor exposure | Subs are rarely the bond principal but may be named or required to show surety capacity on public bids. |

| Payment protection source | Subcontractors rely on the payment bond, not the bid bond, for protection against nonpayment. |

| Bonding sequence | Bid bond covers the bidding phase only; performance and payment bonds take over after contract award. |

| Practical preparation | Review full bid documents, prepare financial records early, and know your bonding limit before pursuing bonded work. |

Why subcontractors who ignore bid bonds pay for it later

I have watched subcontractors lose significant opportunities because they treated bid bonds as the prime’s problem and tuned out. That attitude costs money in ways that are not always obvious until the damage is done.

The scenario I see most often: a sub prices a public project, the GC wins the bid, and then the surety asks for the sub’s financial statements because the sub is named for a major trade package. The sub scrambles, the documents are incomplete, and the surety either delays the bond or asks the GC to find a replacement sub. The original sub loses the work, and the GC loses confidence in them for future bids.

What I have found actually works is treating bonding capacity as a business asset you actively manage, not a bureaucratic hurdle you clear once a year. Subcontractors who maintain clean financials, communicate proactively with their surety broker, and read bid documents thoroughly before pricing consistently win more bonded work than their competitors. They also avoid the painful experience of being replaced on a bid they helped price.

The other insight worth sharing: your bonding history is a reputation signal to general contractors. Primes who know you are bondable, financially stable, and easy to work with during the surety process will bring you into bids earlier and advocate for you with their sureties. That relationship compounds over time in ways that raw bid pricing never can.

— Jen Reese

How Won2Build helps subcontractors stay on top of bid requirements

Tracking bonding clauses, bid deadlines, and subcontract requirements across multiple active bids is exactly where details fall through the cracks. Won2Build’s Bid Track software gives subcontractors a centralized pipeline to manage every active bid, flag bonding requirements, and track submission deadlines without juggling spreadsheets or email threads. The platform connects directly to Won2Build’s full construction software suite, so the data you enter at the bid stage flows through to project management without re-entry. For subcontractors competing on bonded public work, that kind of organized bid management is not a convenience. It is a competitive advantage. Explore the full Won2Build product suite to see how each tool supports your business from first bid to final payment.

FAQ

What is a bid bond in simple terms?

A bid bond is a guarantee that a contractor will honor their submitted bid price and provide the required performance and payment bonds if they win the project. If the contractor refuses or cannot deliver those bonds, the project owner can file a claim against the bid bond.

Do subcontractors need their own bid bonds?

Most subcontractors do not post bid bonds themselves. However, some public project bid documents require subcontractors to be named on the prime’s bond or to provide proof of surety capacity at bid submission, so reading the full bid document is critical.

What is the difference between a bid bond and a payment bond?

A bid bond protects the project owner during the bidding phase by guaranteeing the contractor will sign the contract. A payment bond protects subcontractors and suppliers during construction by guaranteeing they will be paid for their labor and materials.

When does a bid bond claim actually occur?

A bid bond claim occurs after award if the winning contractor refuses to sign the contract or cannot provide the required performance and payment bonds. Claims are not triggered by construction performance issues or subcontractor nonpayment.

How does a subcontractor’s bonding capacity affect bid opportunities?

A subcontractor’s bonding capacity functions as a financial prequalification. General contractors and their sureties may require proof of bonding capability before naming a sub on a bonded bid, and subs who cannot demonstrate adequate financial strength risk being replaced before the bid is submitted.

Recommended

One login for estimating, bid tracking, change orders, and labor.

The Hub is free. Pay only for the apps you turn on.

Create your free Hub account- The Role of Estimate Templates for SubcontractorsDiscover the vital role of estimate templates for subcontractors. They streamline bids, protect profits, and enhance professionalism. Learn more!

- The Role of Electronic Time Tracking for Construction ProjectsDiscover the role of electronic time tracking in construction projects. Improve accuracy, compliance, and efficiency while saving time and money.

- How to Set Up Project Budget Tracking for ContractorsLearn how to set up project budget tracking effectively. Avoid costly surprises and ensure project profitability with our comprehensive guide.